This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

A new investigation into Floridas property insuranceindustry is set to begin, raising significant questions about insurer profitability, financial transparency, and the true reasons behind skyrocketing premiums for policyholders.

property/casualty insuranceindustry recorded a net underwriting gain of $3.7 “After years of consistent losses, premium growth is helping the overall … billion and net income of $94.6 billion for the first-half of 2024, according to a new report.

The global economy is increasingly interconnected, and even in industries like insurance, global issues like supply chain challenges, tariffs, and trade agreements can have significant impacts. While the relationship between tariffs and insurance costs can seem unrelated, tariffs can increase costs for insurers and policyholders.

Among the initiative’s goals is aggregating more data from insurers to better understand challenges to affordability and availability on state levels, which the NAIC can then translate into actionable policy proposals. We’re talking about why premiums are where they are.”

Tort reform is discussed as a legislative solution to the challenge of legal system abuse excessive policyholder or plaintiff attorney practices that increase costs and time to settle insurance claims. At least 38 of those events happened in the last five years, with 14 in 2023.

Zywave, a leading insurance technology provider, today announced its 2025 Summer Launch, introducing a suite of advancements designed to drive profitable growth and empower insurers and brokers in an environment of escalating risk.

Only 30 percent are aware of premium savings for implementing mitigation measures. Seventy percent revealed they would be willing to pay higher premiums for better protection against future severe weather events. Policyholders lose the ability to work through and settle the claim efficiently. However, the U.S.

As high-severity natural catastrophes wildfires, floods, hurricanes, and others become more frequent and more people move into riskier locales, insurance affordability and availability have become a challenge in many states. For many, this insurer of last resort has become the insurer of first resort.

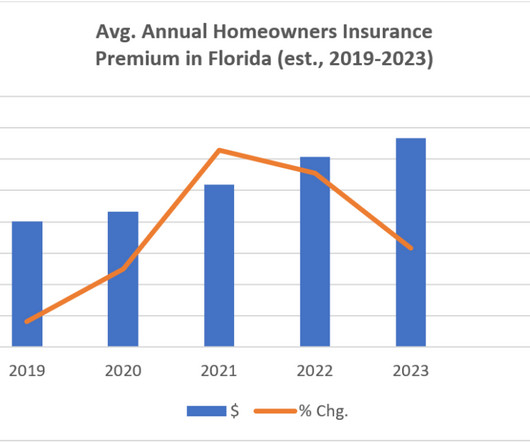

Homeowners insurancepremium growth in Florida has slowed since the state implemented legal system abuse reforms in 2022, according to a Triple-I analysis. As shown in the chart below, average annual premiums climbed sharply after 2020. In 2022, average homeowners premium rates rose more than 17 percent, to $3,040.

Disability Insurance Rates By Benefit Period How Much Is Benefit Period in Disability Insurance a Month? The cost of disability insurance by benefit period can vary. Heres a quick look at how different benefit periods can affect your monthly premiums. Heres how different occupations might affect your premiums.

One of the most challenging and unpredictable issues facing the insuranceindustry lately is social inflation. This trend describes the phenomenon of unexpected rising insurance claim costs because of societal trends and views toward litigation.

The insuranceindustry is undergoing a fundamental transformation. Insurers, agents and brokers are grappling with rapidly evolving risks that are becoming increasingly complex. In this intensifying risk trajectory, outperformance wont come from raising premiums, acquisitions, or continuing with business as usual.

However, this is a general estimate, and your actual premium may be higher or lower based on factors such as your deductible choice and any additional coverage options you select. Condo Insurance Rates By Deductible Choice How Much Is Deductible Choice in Condo Insurance a Month?

AI has rapidly transformed the insuranceindustry and more changes will continue as the technology and use cases mature. New efficient processes and workflows for underwriting, claims, policy administration, billing, and customer service have been implemented across the industry.

The homeowners insurance market is complicated and dynamic, and many policyholders have experienced increased rates in recent years despite no changes to their coverage or claims filed. Even among typical homeowners policies, premiums likely increased year over year. Reduce liability risks. Explore discounts. 3 or 5 years).

Emerging Property Insurance Trends 2024 Welcome to our guide on emerging trends in the property insuranceindustry. As we dive into the evolving landscape of property insurance, it’s important to stay informed about the latest trends and challenges affecting the market.

The Importance of Consumer Education Consumer education is a critical aspect of making informed decisions regarding insurance coverage and navigating the complexities of the insuranceindustry. By gaining insurance knowledge , individuals can protect their property effectively and avoid falling victim to insurance scams.

2025 will bring new ideas, innovations, and changes to an ever-evolving insuranceindustry. Driven by rapid advancements in technology, shifting risks, and increasing policyholder expectations, the industry will likely have different products and services by the time 2025 draws to a close.

Severe weather is transforming the auto insuranceindustry. This means insurers must adapt to changing weather patterns and increasing unpredictability. Focused on the impacts of severe weather events on the auto insurance and repair industries, the report gives timely details on the future of the industry.

As we’re trying to raise awareness of this problem with consumers, ‘social inflation’ doesn’t work,” said discussion moderator and Triple-I’s Chief Insurance Officer Dale Porfilio. Louisianans Need to Know Legal Reforms Boost Florida Insurance Market; Premium Relief Will Require More Time How Georgia Might Learn From Florida Reforms U.S.

Allstate, a household name in the insuranceindustry, is now bringing its trusted reputation to Medicare Supplement (Medigap) plans. With decades of experience providing peace of mind to millions of policyholders, Allstate has created Medigap plans that offer comprehensive coverage, flexibility, and affordability.

This era gave rise to specialised insurance products, covering factories, railways, and an expanding workforce. By the 20th century, the insuranceindustry began to reflect broader societal shifts. This transparency builds trust between insurers and policyholders, as all parties have access to the same information.

Businesses may end up with inaccurate ITV calculations for a wide range of reasons — whether it stems from ineffective property valuation methods, intentionally underestimating costs to secure reduced premiums or being impacted by factors outside their control (e.g., inflation). Regardless, such inaccuracies are all too common.

What is gamification and how does it relate to the insuranceindustry? In the insuranceindustry, gamification can be used to enhance customer engagement, boost sales performance, and improve customer loyalty and retention. What is gamification in insurance? How can gamification help insurance companies?

However, email marketing stands out as a crucial tool for the insuranceindustry. With its ability to directly reach current clients, potential leads, and past policyholders, email marketing provides a platform for personalized, timely, and relevant content delivery. Treating them all alike can lead to missed opportunities.

It’s a double play—claims processed swiftly, premiums collected seamlessly, and customers satisfied. The insurance infield turns grounders into outs, just as MLB infielders turn hits into double plays. For insurers, the grand slam is an exceptional customer experience with optimized operations. The ball never hits the dirt.

For example, a blog feature on life insurance may begin by differentiating term and whole life insurance before delving into specifics such as guaranteed whole life or indeterminate premium whole life. Insight into local insurance requirements Insurance requirements vary dramatically from one state to the next.

FIA Accumulation Highlights : Review premium requirements, fixed rates, withdrawals and more! Fixed Annuity Highlights : Inform your customers on current yields, first year bonus rates, minimum premiums and more! There are 3 common types of annuities that life insurance agents sell. Download Current Annuity Rates Now!

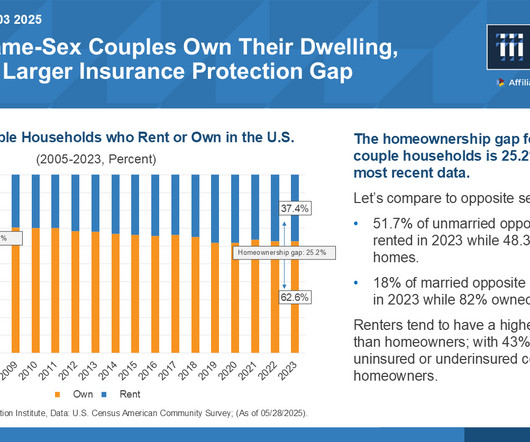

Thus, homeownership status can drive participation in the insurance market. Examining factors that impede homeownership for same-sex couples might shed light on how to attract and retain more policyholders in this demographic. percent of residents pay more than 30 percent of their income) and San Francisco (37.6 percent of residents).

The third paper – “ Balancing Risk Assessment and Social Fairness: An Auto Telematics Case Study ” – explores the possibility of using telematics and usage-based insurance technologies to reduce dependence on sensitive information when pricing insurance.

In today’s rapidly evolving world, the insuranceindustry stands at a critical juncture. Zywaves new Navigating the Escalating Risk Trajectory Report provides a comprehensive analysis of these dynamic forces, urging insurers and brokers to adapt swiftly and strategically. Read the full report here. Looking for solutions?

President Donald Trump are on track to increase the price of parts and materials used in repairing and restoring property after an insurable event. Analysts and economists, predict these price hikes will lead to higher claim payouts for P&C insurers and, ultimately, higher premiums for policyholders.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content