This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In this final part of our series exploring the nine elements of independent premium audits, we turn our focus to specialized situations and nuanced adjustments auditors carefully evaluate. Auditors disallow estimates, making precise documentation vital to receiving the intended premium savings associated with this exception.

A Business Owners Policy, commonly known asa BOP bundles essential protections like property, general liability, and liquor liability into one streamlined solution. What is a Business Owners Policy (BOP)? A BOP is an efficient way to safeguard against these operational risks with one comprehensive policy.

However, this market comes with its own set of challenges, including price sensitivity, unique underwriting processes, and sometimes, a lack of awareness among consumers. Key products to consider include: Whole Life Insurance : A staple for final expense agents, it provides lifelong coverage at affordable premiums.

The Birthday Rule is gaining traction across the country, allowing Medicare Supplement policyholders to switch plans without medical underwriting around their birthday each year. Reduced underwriting can lead to higher premiums , increased policy lapses, and fewer carriers remaining in the market. in 2024 vs. 13.0%

Rising expenses could perhaps cause higher insured values, leading to policy adjustments and higher premiums. Many industries are feeling the uncertainty of tariffs and changing trade policies, which can make underwriting more challenging and pricing less certain. Education is often the first step.

point enhancement compared to the prior year and representing the sector’s most favorable underwriting performance since 2013, as detailed in a recent report by Triple-I and Milliman. This advancement was largely attributable to robust net written premium (NWP) expansion, with growth rates of 14.4 demonstrating a substantial 5.1-point

Policy Information Details of the insurance policies under which the claims were filed. Insurance companies rely on these reports to assess risk when underwriting a new policy. The most common report is the Comprehensive Loss Underwriting Exchange (C.L.U.E.) report, managed by LexisNexis.

At the point of purchase the exact moment when customers are most receptive to considering protection insurance providers are now able to make instant underwriting decisions. At the same time, they benefit from contextual data that improves underwriting precision. Certain types of non-complex commercial insurance are also in scope.

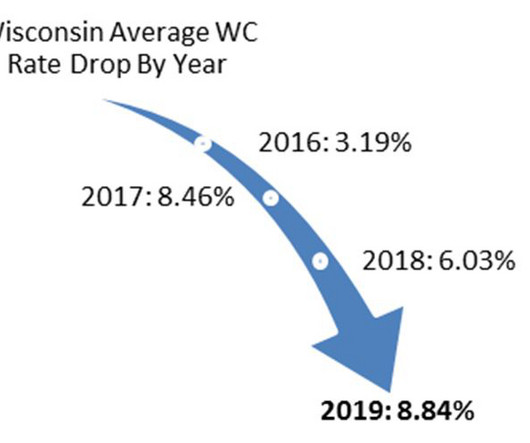

This rate reduction will affect work comp policies with renewal dates between 10/01/24 to 09/30/25. Workers compensation rates are state mandated in Wisconsin, meaning all insurance carriers must use the same rates resulting in premiums from one carrier to another are basically the same. Rates in 2024 fell an average of 10.5%

For insurers, this means two things: Stricter policy requirements to ensure businesses meet minimum security standards. Insurers are also refining their underwriting processes, using AI-driven analytics to move away from traditional questionnaires and toward real-time risk assessments that adapt to a companys evolving cyber posture.

Automatic renewal: Ensures continuous coverage with hassle-free policy renewals. These advantages make Distinguisheds policies a comprehensive and flexible solution for Chicago landlords. These advantages make Distinguisheds policies a comprehensive and flexible solution for Chicago landlords.

In Los Angeles, housing code violations present challenges that affect property safety, compliance, and insurance underwriting. Even if some violations are eventually addressed, a history of non-compliance can still lead to higher premiums. Can you outline some of the most common housing violations in Los Angeles? Yes, indeed.

When discussing final expense insurance with clients, agents often encounter misconceptions that can prevent clients from seeing the value of these policies. With this policy, you’re securing a fund for your family, so they don’t have to worry about the financial side during a difficult time.”

Businesses with mobile property whether equipment, materials, or cargo need protection beyond standard policies. Distinguisheds inland marine policies provide tailored protection, ensuring businesses can recover quickly and maintain operations with minimal disruption. Who Needs Inland Marine Insurance?

Introduction to Final Expense Insurance Final Expense Insurance is a small whole life insurance policy designed to cover end-of-life costs, such as funeral expenses, medical bills, and other outstanding debts. Recurring Revenue: Final Expense Insurance policies provide agents with consistent commissions, creating a stable income stream.

TGS Insurance » Blog Homeowners Insurance Underwriting Questions: What to Expect When Getting a Quote So, you’re ready to take the plunge into homeowners insurance. Maybe you’ve just bought a new home, or maybe it’s time to revisit your current policy to make sure you’re covered in all the right places. Location is everything.

From understanding local exposures to leveraging tailored package policies, youll gain the insider knowledge needed to win your clients trust and business. High-limit umbrella insurance: Offers liability coverage beyond standard policy limits, with options up to $130 million. What Exposures Do Charlotte Restaurants Need to Worry About?

Not only are they insured in the event of a covered risk, but they can also sleep well at night knowing they have a policy limit that is high enough to cover whatever gets thrown their way. This allows the owner-occupant to insure both the building and their personal unit under the same policy.

Even if some violations are eventually addressed, a history of non-compliance can still lead to higher premiums. Both resolved and unresolved violations can affect the terms, premiums, and overall coverage of these policies. She oversees the programs strategic planning, product management, and underwriting profitability.

But with value comes risk, and standard homeowner insurance policies frequently fall short when it comes to protecting one-of-a-kind instruments. Thats why a specialized collectibles policy is the right solution for clients who own rare, high-value guitars whether theyre collectors, professional musicians, or investors.

Even if some violations are eventually addressed, a history of non-compliance can still lead to higher premiums. Both resolved and unresolved violations can affect the terms, premiums, and overall coverage of these policies. She oversees the programs strategic planning, product management, and underwriting profitability.

A policy can help with incident-related costs, but it wont stop attackers from penetrating your environment. Cowbell MDR SOC-as-a-Service actively works to reduce your risk and mitigate incidents before they cause damageoften lowering your insurance exposure and premium over time.

They can be set by central banks and are influenced by several factors, including inflation, economic growth, and monetary policy decisions. Sometimes, changes in global financial markets or government policies can also be catalysts for rate hikes. Here’s how: insurers rely on investment income to keep premiums competitive.

With infractions ranging from heating failures to illegal conversions, understanding these issues is essential for assessing risk and underwritingpolicies. Even if some violations are eventually addressed, a history of non-compliance can still lead to higher premiums. Katie is based in Rhode Island.

Even if some violations are eventually addressed, a history of non-compliance can still lead to higher premiums. Both resolved and unresolved violations can affect the terms, premiums, and overall coverage of these policies. She oversees the programs strategic planning, product management, and underwriting profitability.

Zywave’s proprietary data tools are designed to help you improve your underwriting efficiency, refine your rates and better educate policyholders on the risks they may face. With Client Engagement Suite , you can engage your policyholders throughout the policy lifecycle on all things cyber.

Insurance Company: The Risk Bearer Often referred to as the underwriter, insurer, or carrier, the insurance company provides the workers’ compensation policy and assumes the employers risk. Employers bear financial responsibility for premiums and retained losses, emphasizing the importance of proactive risk management.

Caroline Thompson, Chief Underwriting Officer added, “Cowbell’s underwriting process integrates data points from security tools and application questions. This results in lower premiums, better coverage, and higher policy limits.” This results in lower premiums, better coverage, and higher policy limits.”

And get this some even let you pay as you go instead of heavy annual premiums. Limitations and Challenges Faced Through Traditional Insurance Model Traditional insurance operates on a principle of risk pooling, where many pay premiums to cover the potential claims of a few. Every person, every business, every situation is different.

To feel confident in your policy before you sign, make sure you understand how to read a homeowners insurance quote. Quotes that are ready quickly are usually based on a small subset of information, then the initial baseline quote is refined during the underwriting process. You only pay when purchasing the policy. Deductibles 8.

Inflation drives up property valuations , construction costs , and insurance premiums. This has resulted in higher premiums and limited coverage in catastrophe-exposed areas. Insurers are investing in advanced technology and data analytics to improve risk assessment and underwriting processes.

Many insurance carriers use third-party crime scores to evaluate their exposure to criminal risk when underwriting general liability insurance policies. Thus, affordable housing providers are highly likely to experience a loss of coverage or relatively high insurance premiums.

Unsafe driving, inflation, and auto repair costs are responsible, in part, for rising premiums. We can see how insurance premiums are affecting the gulf coast and now, California. It is even likely in some cases that their insurers understood these efforts and lowered their premiums. during this 10-year period. [iv]

” or can’t get the insurance you deserve for that matter – insurance with reasonable premiums and without unnecessary restrictions. In other cases, it will be due to underwriting appetite of insurers and their ever changing attitudes to risk. It can be an extremely nuanced subject & question.

If an MGA specializes in unique commercial policies, the survey might ask about coverage satisfaction and growth potential within that niche. For example, asking if a carrier’s underwriting support is a deciding factor or if digital tools play a significant role helps carriers understand which attributes matter most.

You will want to make sure you have the right policy in place that will cater for your particular requirements. It is also important that you inform your insurer that the property is empty, as there are some important conditions that you will need to comply with to ensure your policy remains valid.

Unfortunately, these unique risks are rarely appropriately covered by standard homeowner insurance policies. Avid collectors who rely on their homeowner’s policy are likely to encounter low coverage limits — if their collectibles are covered at all. For most, this will mean a collectibles policy.

Our Builder’s Risk policies come standard with all of the most important coverages your clients will need to protect their under-construction properties. Distinguished’s Builder’s Risk Insurance policies are customized based on the needs and situations of your clients. How Much Does Builder’s Risk Cost in Georgia?

However, if your clients have been lucky enough to come across a rare Illustrator Pikachu Card ( worth over $550,000 ) or a vintage Boba Fett toy ( worth over $500,000 ), they’re going to need an insurance policy that properly covers them. This means a specialized collectibles policy. How Do You Insure a Toy Collection?

Let’s explore how and why your credit score affects your home insurance , what insurers are really looking at, and what you can do to keep your premiums manageable. However, in most states, your credit score can significantly influence your premiums. Now, you might be wondering just how much your credit score can affect your premium.

The South Carolina Wind and Hail Underwriting Association, also known as Wind Pool, is an association of insurance providers. With replacement cost coverage, a flood policy must also be active at the time of the damage, or else there will be actual cash value coverage. This covers any damage caused by wind or hail events.

If we are comfortable with our exposure, we may consider increasing the AOP deductible and the theft deductible , depending on the underwriting analysis. Are there any emerging trends in the construction industry that are impacting builder’s risk underwriting? We bound the policy for a six-month term, and the premium was $1,300.

In fact, medical underwriting hasn’t been used for individual/family health insurance policies since 2013. For individual/family major medical policies with effective dates of 2014 or later, the insurer cannot take the applicant’s medical history into consideration. Here’s how income is calculated under the ACA ).

Life insurance often feels like a topic best tackled earlier in life, but its far from being too late for seniors to secure a meaningful policy. The Growing Demand for Senior Life Insurance With people living longer than ever, the demand for senior-specific life insurance policies is growing.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content