This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

InsuranceCarriers are reducing their appetite for risk and increasing premiums. This means they are being much more selective in what they are willing to insure. This post is part of a series sponsored by TSIB. If they are going …

New high net worth (HNW) insurancecarriers were entering the market. Established underwriting operations had become a consistent source of profits for investors and parent companies. The year was 2016. Aging brokerage owners with sizable private client books of business …

So you have taken your insurance exam and got a license to sell insurance. Now, you want to start selling insurance? Before you do, you need to get an insurancecarrier appointment. What is an insurancecarrier appointment? How to get a direct insurancecarrier appointment as a new agent?

As cyber insurance rates have begun to stabilize, insurancecarriers are seeking more diversification to fuel their underwriting and growth strategies, according to panelists at this year’s PLUS Cyber Symposium in New York City. “They’re seeking diversification in the standard …

In this 45-minute discussion, industry experts explored how the collaboration between Zywave and Verisk is bringing ISO Electronic Rating Content™ (ISO ERC™) into the ClarionDoor platform to help insurancecarriers simplify underwriting, improve rating accuracy, and drive better business results.

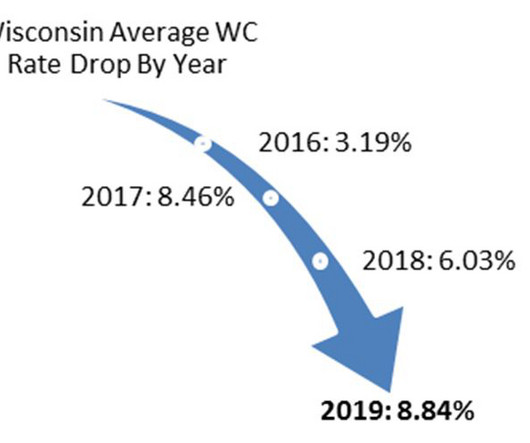

Workers compensation rates are state mandated in Wisconsin, meaning all insurancecarriers must use the same rates resulting in premiums from one carrier to another are basically the same. This rate reduction will affect work comp policies with renewal dates between 10/01/24 to 09/30/25. What can Contractors do?

However, this market comes with its own set of challenges, including price sensitivity, unique underwriting processes, and sometimes, a lack of awareness among consumers. When you partner with FEB , youll gain access to over 15 highly rated life and health insurancecarriers, ensuring you have a comprehensive portfolio for your clients.

Many insurancecarriers use third-party crime scores to evaluate their exposure to criminal risk when underwriting general liability insurance policies. The post How InsuranceCarriers Use Crime Scores to Assess Risk in the Affordable Housing Industry appeared first on Scott Insurance.

A Managing General Agent (MGA) is a specialized type of insurance intermediary that has underwriting authority granted by an insurer. Unlike agents or brokers, MGAs can bind coverage, price policies, and handle claims they essentially act as an extension of an insurer. How do MGAs Differ From Insurance Brokers?

Navigating the insurance landscape can be challenging for insurance agency owners. From understanding various acronyms and abbreviations like IMO, FMO, and MGA, to managing relationships with insurancecarriers, there is a lot to consider. Frequently Asked Questions What is an IMO in insurance? Yes, I need an IMO!

Dan brings over 25 years of extensive experience and leadership expertise within the Property and Casualty insurance sector. Prior to joining Agency Revolution, Dan spent 20 years at Nationwide where he served in management roles for commercial underwriting, loss control, sales automation and technology, and business architecture.

InsuranceCarrier The carrierunderwrites the policy and carries the financial risk for claims (in guaranteed cost programs). They’re also known as the insurer or underwriter. Key Players in the Workers Comp Ecosystem Heres a closer look at the major participants and how they fit into the puzzle: 1.

Causes of the challenging property insurance market include: Higher rates of inflation and construction costs which are driving significant replacement cost increases. Uneven investment profits causing insurers to pursue underwriting profit, which translates to stricter underwriting criteria and declined submissions.

Many industries are feeling the uncertainty of tariffs and changing trade policies, which can make underwriting more challenging and pricing less certain. This could cause higher rates in commercial property and homeowners lines. This could create the need for frequent rate changes, adding to consumer uncertainty.

Insurance Company: The Risk Bearer Often referred to as the underwriter, insurer, or carrier, the insurance company provides the workers’ compensation policy and assumes the employers risk. Lets explore the roles of these critical players in a workers’ compensation system.

Dan brings over 25 years of extensive experience and leadership expertise within the Property and Casualty insurance sector. Prior to joining Agency Revolution, Dan spent 20 years at Nationwide where he served in management roles for commercial underwriting, loss control, sales automation and technology, and business architecture.

TGS Insurance » Blog What Is a Homeowners Insurance Quote? A homeowners insurance quote is the proposed amount that you would pay an insurancecarrier to cover your home. The quote will be based on many factors, including your home’s age, building features, location and size, as well as your insurance score.

In 2018, the 5 th Circuit Court of Appeals took things a step further in Certain Underwriters at Lloyd’s of London v. In that case, a hotel filed a lawsuit against its insurer for refusing to cover hail-related roof damage under a commercial property insurance policy. Lowen Valley View, L.L.C.

Continue reading to enhance your efforts to sell P&C insurance right from the comfort of your own home. Trends in Property and Casualty Insurance Most insurance companies are making the underwriting and policy issuance process simpler and more streamlined. Overall, premiums have become less expensive as well.

TGS Insurance » Blog With hurricane season in full force, South Carolina residents living on the coast must protect their homes from the upcoming storms. Understanding how windstorm insurance works in these areas is the first step in adequately protecting your home. Why Would I Have to Get South Carolina Wind Pool Insurance?

In California and other high-risk areas, carriers may offer geospatial mapping tools and other solutions to help mitigate and manage wildfire exposures. Proactively solve problems alongside carrier partners. Position your agency as a valuable and reliable partner to strengthen relationships and improve outcomes when working together.

An FMO provides insurance brokers with support and connects them with a roster of insurancecarriers – offering a range of products and services. A 2024 article published by PeopleKeep features an overview of FMOs and the role they can play for insurance professionals.

Material Change in Risk Manufacturers & Distributors should prepare for the possibility of increased underwriting scrutiny. Materially modifying production and assembly lines to provide desperately needed PPE products could change risk considerations and impact an organization’s insurability.

Insurance companies recognize the imperative to invest in modern digital technologies to achieve their goals of cost reduction and revenue growth. Insurancecarriers recognize the importance of investing in future-proof architecture, characterized by open APIs and low-code systems that easily integrate into broader technology ecosystems.

Consequently, this compounds and drives up the average D&O Insurance premiums specific to these sectors. 2024 Outlook for D&O Premiums As 2024 approaches, the D&O Insurance market anticipates continuing from a once-volatile rate environment to more stable conditions.

. “Insureds need to be aware of the potential risks they face and work closely with their insurers to understand the coverage limitations and take proactive measures to protect their properties.” Insurers are investing in advanced technology and data analytics to improve risk assessment and underwriting processes.

For example, ask about their current insurance plan (if any) and any issues they have encountered while covered under that plan. It’s important you create a connection with your customers, so they believe you are working for them – not for yourself and not for the insurancecarriers.

It allows you to inform them about what is happening in real time in your state insurance market. Simply communicating to your customers that rates are up, underwriting is tightening, or an insurancecarrier is pulling out of a state is a great way to be proactive. Aim to get 3-10 new Google reviews per month.

When a project is under construction or renovation, your clients are likely not covered by their homeowner’s insurance or business insurance. Different Builder’s Risk insurance policies vary from one insurancecarrier to another. This is where Builder’s Risk becomes essential.

Furthermore, most broker services are free to consumers since brokers are compensated by insurancecarriers. The Role of Health Insurance Brokers in the Market Health insurance brokers play a pivotal role in the health insurance market, acting as a crucial link between consumers and insurance companies.

If we don’t get down to addressing the loss ratio — underwriting, pricing, risk selection, and claims management — for many carriers, even if they cut costs by 100%, they’re still not going to be profitable. This isn’t just because of the size of their expense ratio.

By Elizabeth Blosfield As cyber insurance rates have begun to stabilize, insurancecarriers are seeking more diversification to fuel their underwriting and growth strategies, according to panelists at this year’s PLUS Cyber Symposium in New York City. “They’re seeking diversification …

While some insurance companies in Florida and beyond have balked at writing properties with rooftop solar panels, FM Global says it has pioneered an idea that may help a testing system that certifies panels for fire and hail resistance.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content