This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The New Jersey Supreme Court recently ruled that an insurer had no duty to defend an insured employer against an injured employee’s personal injury lawsuit alleging negligence and intentional harm. The high court found that Hartford Underwriters Insurance Co. was …

When a workplace injury occurs, most people think of two parties: the injured worker and the employer. Insurance Carrier The carrier underwrites the policy and carries the financial risk for claims (in guaranteed cost programs). They’re also known as the insurer or underwriter.

However, the insurers underwriter reviews this assignment to confirm its appropriateness and may suggest alternative classifications if discrepancies or better-fitting categories exist. If the underwriter identifies a different classification as more suitable, they notify the broker and employer.

Carrier adjustments reflect underwriting discretion, including credit for safety programs. Injury response scripts: Reinforce during claims that the employer is covering their wages and care. Key areas where employer leadership matters: Injury response : Fast, supportive responses reduce litigation and speed up healing.

Why Restaurant Need a Business Owners Policy Restaurants are fast-paced, high-risk environments that face frequent challenges from customer injuries and equipment breakdowns to power outages and spoiled inventory. fire suppression, alarms) Distinguished also provides access to underwriters who specialize in hospitality risks.

This repeated exposure to risk increases the likelihood that larger claims might occur in the future, which alarms underwriters. Underwriters view very large losses as rare and unlikely to repeat. When an organization experiences many smaller claims, it suggests that workplace hazards are not being effectively addressed.

Additionally, there will be increased scrutiny for communities that are in the areas surrounding these facilities as there is an increased bodily injury component due to potential impact to humans. The lawsuits are mainly related to bodily injury claims for both workers and people in the surrounding communities who have developed cancer.

For example, a resident suffered severe injuries a fractured tibia and fibula after slipping on black ice while walking to her car. It covers physical damage to the other vehicle, bodily injuries, medical expenses for anyone injured (other than the insured driver), and legal expenses if the insured is sued for negligence.

Insurance Company: The Risk Bearer Often referred to as the underwriter, insurer, or carrier, the insurance company provides the workers’ compensation policy and assumes the employers risk. These benefits include medical coverage, wage replacement, and rehabilitation services for work-related injuries or illnesses.

Slip-and-fall incidents: High foot traffic in dining areas and restrooms increases the risk of customer or employee injuries, which can lead to costly liability claims. General liability insurance: Coverage for legal claims related to customer injuries or property damage.

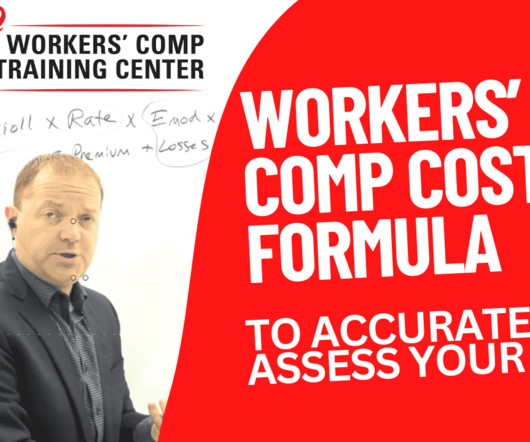

So this is your premium adjustments, and these are discretionary adjustments that can be given by your underwriter based on how well they perceive you managing your risk, how well they perceive you managing your risk. Stack is the creator of Injury Management Results (IMR) software and founder of Amaxx Workers’ Comp Training Center.

Broad risk coverage: Protects landlords from tenant injuries, property damage claims, and other liability concerns beyond standard policies. Receive a quote: Our underwriting team will review your submission and provide a competitive, bindable quote. How to get started: Register with us : Gain access to our landlord insurance programs.

General liability: Protects against tenant or visitor injuries, legal claims, and medical expenses. Receive a customized quote: Our underwriting team evaluates each submission to provide bindable quotes. Loss of rental income: Replaces rental income if a covered event makes the property uninhabitable.

These legal factors are critical when it comes to determining liability in cases where unresolved violations have led to damages or injuries. She oversees the programs strategic planning, product management, and underwriting profitability. Katie is based in Rhode Island.

Another company may have an unusually high experience modification rate that they want to bring down by reducing the frequency of worker injuries. The claims review should be designed to account for how frequency and severity may affect underwriting decisions so that the policyholder can move toward its coverage objectives.

These legal factors are critical when it comes to determining liability in cases where unresolved violations have led to damages or injuries. She oversees the programs strategic planning, product management, and underwriting profitability. Katie is based in Rhode Island.

These events may include property damage, liability claims from work-related injuries, break-ins, or business interruption. Liability Coverage Commercial insurance also includes liability coverage, which protects businesses from legal claims and lawsuits alleging property or physical injury.

Environmental / Pollution Environmental/pollution policies are available in the market and can contemplate both the first party (property) and third party (general liability – bodily injury/property damage) mold exposure.

This unique handbook on the issues of employment in the context of work-related injuries features the relevant statutes, regulations, and case law that has developed pertaining to the issue of whether a worker is an employee or independent contractor.

” In response to rising property losses, insurance companies have adjusted their underwriting guidelines, resulting in higher premiums and limited coverage for properties located in high-risk areas. Insurers are investing in advanced technology and data analytics to improve risk assessment and underwriting processes.

Louisiana recently enacted a law enforcing some oversight over TPLF, Temple noted, as well as repealed a unique “three-year rule” that impeded actuarially-sound underwriting. But as the state’s bodily injury claims climb well over the national average, more reform is needed to return insurance profitability to the state.

These include: Damage done intentionally to a covered item Injuries to employees working on the project Costs related to manufacturing defects Damages related to terrorism, nuclear attacks, or military actions Other policies should offer coverage for some of these risks. Our Builder’s Risk program does not cover some specific risks.

Premises liability claims : Legal expenses and liability coverage related to any injuries, including trips and falls, that occur on the site. Errors or omissions in their work could cause costly mistakes, injuries, or property damage. Materials : The loss of building materials that are on the site or in transit between covered sites.

The CLAIM Act would let these businesses obtain insurance to cover the same risks of theft, damage, injury, loss, and liability as all other businesses. Easier to operate Passage of these laws would make it easier for cannabis-related businesses to operate.

Quotes that are ready quickly are usually based on a small subset of information, then the initial baseline quote is refined during the underwriting process. Coverage F ( Medical Payments ) : The amount your insurance carrier will pay for medical treatment of injuries that happened at your homesite falls under this coverage.

Homeowners insurance is a crucial financial safety net for homeowners, providing protection in the event of property damage, loss of personal belongings, or liability for injuries that occur on the premises. What is Homeowners Insurance? Furthermore, technological advancements have also played a role in shaping the insurance industry.

Additionally, it can provide coverage for business interruption, tenant improvements, and liability claims arising from third-party injuries or property damage on the premises. It protects against perils like fire, explosions, storms, and other risks outlined in the policy.

It also includes auto liability coverage for costs related to property damage or injuries caused by a crash. Slips and Falls Swimming pools and spas are a major selling point for hotels, but theyre also hotspots for accidents, injuries, and lawsuits. Garagekeepers : A policy that covers cars parked by the hotels valet service.

If no benefits are being paid on account of an injury, counsel for the injured worker should name the PEO or employee leasing company, the special employer and its insurer, and any servicing agent of the PEO and their insurer as parties because there is joint and several liability between the general and special employers.

In recent years, it has been the most profitable property/casualty line of business, having experienced its sixth consecutive year of combined ratios under 90 and its ninth straight year of underwriting gains. A combined ratio below 100 represents an underwriting profit, and one above 100 represents a loss.

With an A&H license, you are generally allowed authority in California to sell products offering coverage for sickness, bodily injury, or accidental death (that may include disability income benefits). The licensee may also transact 24-hour care coverage and Long Term Care insurance.

Under Ohio premises liability law , property owners are frequently held liable for injuries sustained on their properties, making liability coverage crucial. Liability protection: Covers injuries to tenants or visitors, with limits of $1M per occurrence and $2M aggregate. Why Choose Distinguished for Ohio Landlord Insurance?

Rehabilitative and habilitative services and devices (services and devices to help people with injuries, disabilities, or chronic conditions gain or recover mental and physical skills). Small businesses and their employees are no longer subject to medical underwriting for health insurance. Prescription drugs. Laboratory services.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content